€STR Wars: Attack of the Clones

A key feature of exchange-traded futures is that typically nearly all liquidity for a given product is on a single exchange. Liquidity moving from one exchange to another, or on multiple exchanges simultaneously, is a rare occurrence. When liquidity does move from one exchange to another, the results can be rapid and permanent - the collapse of the LIFFE floor when German government bonds moved to Eurex in the late 90s is the classic example.

The recent rise of the futures linked to the Euro short-term rate (€STR) futures contract, with contracts on Intercontinental Exchange (ICE), CME Group and Eurex, is therefore highly unusual. Understanding this liquidity is essential to market participants, in order to minimise the cost of trade, find liquidity and hedge efficiently.

Similar to the transition in the UK from Libor to the Sterling Overnight Index Average (SONIA), Eurozone short-term benchmarks are transitioning from Euribor to €STR. We are now seeing ‘the rise of the clones’ with contracts on ICE, CME and Eurex, all trying to gain liquidity and market share in €STR futures. At the start of November 2023, ICE launched the liquidity program on their €STR future, and here we assess the liquidity and behaviour since the contract launch.

Where are the futures trading?

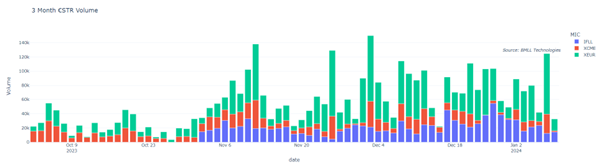

We start by assessing traded volume. We can see that, whilst ICE has had a good market share, it has actually raised volumes in Eurex too, as shown in the below plots.

Fig 1: Traded volumes of €STR futures on ICE, CME and Eurex

Fig 2: Market share of €STR futures on ICE, CME and Eurex

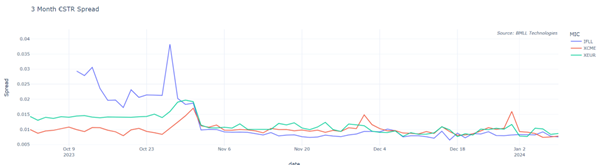

The market share is reflected in the ICE and Eurex spreads, which are tighter than CME on average.

Fig 3: Average spread of contracts of €STR futures on ICE, CME and Eurex.

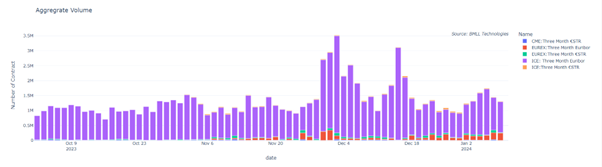

At this point, it is worth noting that Euribor still dominates the overall Euro STR market, and the majority of liquidity is still on ICE Euribor futures. This is because, unlike the other benchmark transitions (such as Libor), there is no deadline for firms to transition from Euribor, and the futures contracts have only recently launched. However, the steady growth of the €STR futures suggests that we will continue to see more liquidity move across to these new products.

Fig 4: Euribor and €STR traded volumes

Going deeper reveals further insights

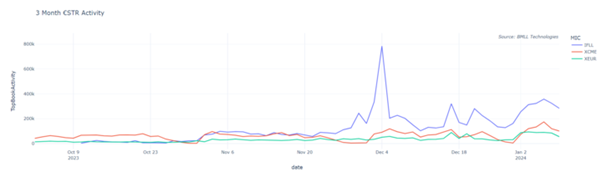

Looking beyond the top of the order book, using Level 3 data, we can gain further insights. If we look at the activity level (defined as the number of updates in the order book), we can see that ICE has significantly more order book updates than Eurex. This possibly suggests a difference in structure between the contracts, or differing participant behaviour.

Fig 5: Activity levels of €STR futures

To understand this further, it is important to note there are unique features for each €STR product. For example, firms trading the CME future can margin offset against SOFR futures (a highly liquid rates future). Similarly, a feature of the ICE product is the ability to trade inter-product spread futures between Euribor (a highly liquid future traded on ICE) and €STR.

Given the difference in order book activity between ICE and Eurex, we can ask an important question - has the €STR-Euribor inter-product spread acted as a source of liquidity on the €STR contract?

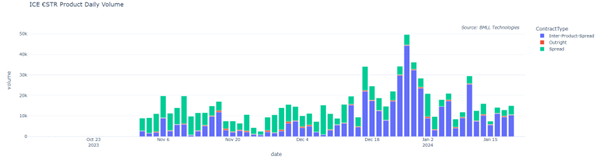

Looking at the data, the answer is yes. First we see that a significant portion of the volume is on the inter-product spread. Secondly, by analysing all ICE €STR futures, we find that more than a third of top of book liquidity on the €STR futures comes from implied orders. Participants are therefore using the inter-product spreads on ICE, which may offer an explanation for the difference in activity between the ICE and Eurex futures. Tracking how this evolves will be important to understand the liquidity on each exchange, especially as volumes grow.

Fig 6: Break down of ICE €STR trading volumes

Understanding where liquidity lies will be crucial

As €STR continues to grow and gain market share, understanding the liquidity profile of competing €STR futures on ICE, CME and Eurex will be critical for market participants to trade better. Whilst it is early days in the battle for this market, already we are seeing differences in liquidity levels, depth of book and trading behaviour across the three markets. Using Level 3 Data, firms can be in a better position to truly understand where to best trade these new futures. The €STR wars have just begun.

- This article is an updated version of an article that was first published on January 18 - data and commentary have been altered to reflect additional analysis

Found this useful?

Take a complimentary trial of the FOW Marketing Intelligence Platform – the comprehensive source of news and analysis across the buy- and sell- side.

Gain access to:

- A single source of in-depth news, insight and analysis across Asset Management, Securities Finance, Custody, Fund Services and Derivatives

- Our interactive database, optimized to enable you to summarise data and build graphs outlining market activity

- Exclusive whitepapers, supplements and industry analysis curated and published by Futures & Options World

- Breaking news, daily and weekly alerts on the markets most relevant to you